Building your home equity boils down to two things: paying down your mortgage principal and increasing your property’s market value. That’s it. These two forces work together to grow the piece of your home you actually own, turning the place you live into one of the most powerful financial assets you’ll ever have.

Your Blueprint For Building Home Equity

Think of home equity as your personal stake in your property. It’s the market value of your home minus what you still owe the bank. When you first buy, your equity is just your down payment. From that day on, your mission, should you choose to accept it, is to grow that number.

This isn’t just about the warm-and-fuzzies of owning more of your house. It’s about building real wealth you can tap into for future investments, handle major life expenses, or simply secure a more comfortable retirement.

We’re cutting through the noise to give you a clear, actionable plan. Forget abstract financial theories. We’re focused on the practical moves you can make—starting today—to make your property work harder for you. You’ll learn how to speed up your ownership timeline with savvy payment strategies and how to strategically boost your home’s value with the right kind of improvements.

The Two Paths to Equity Growth

Building equity isn’t magic. It’s the result of your deliberate actions and the natural forces of the real estate market.

Here’s the game plan:

- Paying Down the Principal: Every mortgage payment you make chips away at your loan balance. Sure, the early payments are heavy on interest, but each one pushes you a little closer to owning your home outright. We’ll show you how to put that process on steroids.

- Market Appreciation: This is the passive side of the game. As property values in your area rise—thanks to demand, economic growth, or new amenities—your home’s value goes up with them. Your equity grows without you lifting a finger.

The real power kicks in when you combine these two forces. By actively paying down your debt while making smart choices that make your home more desirable, you create a compounding effect that can build serious wealth over time.

This guide will walk you through the specifics of both. We’ll cover everything from making extra mortgage payments to identifying high-return renovations that buyers in today’s market are actually looking for.

Before we dive in, if you need a refresher on the basics, check out our guide that explains how to calculate home equity. Whether you’re in a dynamic market like Los Angeles or anywhere else, these principles are your key to turning homeownership into a cornerstone of your financial future.

Your Home Equity Building Toolkit

Here’s a quick overview of the strategies we’ll be covering. Think of this as your menu of options for growing your stake in your property.

| Strategy | What It Is | Best For |

|---|---|---|

| Principal Paydown | Actively paying more than your required mortgage payment to reduce the loan balance faster. | Anyone who wants to own their home sooner and save tens of thousands on interest over the life of the loan. |

| Targeted Improvements | Making strategic renovations (kitchens, baths, curb appeal) that increase your home’s market value. | Homeowners planning to sell in the next few years or those who want to enjoy the upgrades while boosting value. |

| Market Appreciation | The passive increase in your home’s value over time due to location, demand, and economic factors. | Long-term homeowners who bought in an area with strong growth potential. |

| Refinancing | Replacing your current mortgage with a new one, potentially with a lower rate or shorter term. | Homeowners who can secure a significantly lower interest rate or want to shorten their loan term from 30 to 15 years. |

| Adding Income Streams | Renting out a room, building an ADU, or using your property to generate extra cash flow. | Those in areas with high rental demand who can use the income to make larger mortgage payments. |

Each of these tools has its place, and the most effective plan often involves a combination of a few. Let’s get into the specifics of how to put them to work for you.

Accelerating Equity Through Smart Mortgage Payments

It’s easy to see that monthly mortgage debit and just think of it as another bill. It’s not. Every single payment you make is a direct investment in your personal wealth, buying you a bigger slice of your home and turning a liability into a powerful asset.

So why passively follow the standard 30-year plan when you can take control and speed things up?

The secret is in the amortization schedule. Early in your loan, a huge chunk of your payment goes straight to interest. Over time, that balance shifts, and more of your money starts attacking the principal—the actual loan amount. The faster you can force that shift, the faster you build equity and the less you pay in interest over the life of the loan.

Beyond the Minimum Payment

Sticking to the minimum payment is the slow, scenic route to ownership. If you’re serious about building wealth, it’s time to get aggressive. Think of your mortgage principal as a target; every extra dollar you send its way is a direct hit that shrinks your debt and grows your ownership stake. It’s one of the few guaranteed, risk-free returns on your money.

Here are a few straightforward ways to do it:

- Round Up Your Payments: If your monthly payment is $4,825, round it up to an even $5,000. That extra $175 each month goes directly to the principal, quietly shaving years and thousands in interest off your loan without much pain.

- Make One Extra Payment a Year: This is a classic for a reason. You can either save up for a lump sum or, even simpler, divide your monthly payment by 12 and just add that amount to each payment you make. Easy.

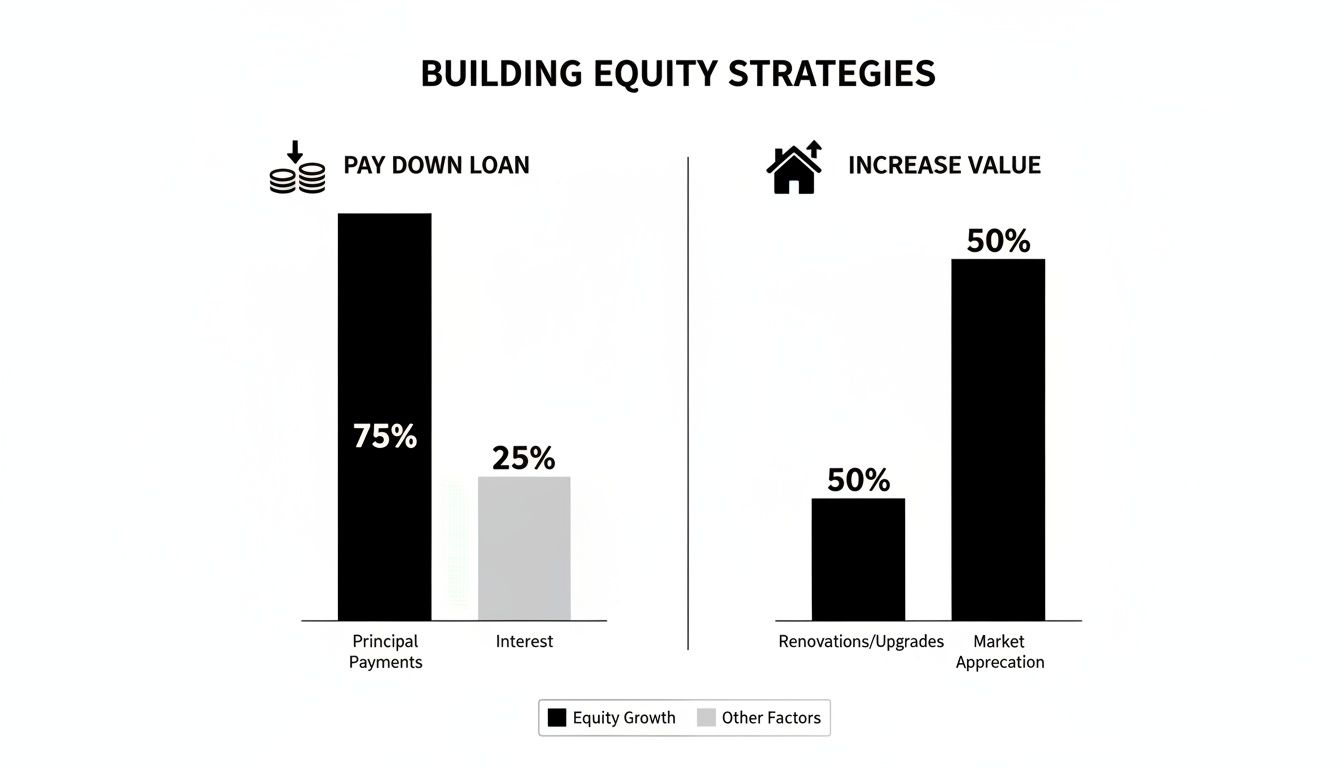

As the chart below shows, you have two main levers to pull: paying down your loan and increasing your home’s value. We’re focused on the first one here—the one you have total control over.

This simple visual highlights that you have both active and passive ways to grow your home’s equity. Let’s stick with the active approach.

The Power of Bi-Weekly Payments

Ready for a more structured, set-it-and-forget-it approach? A bi-weekly payment schedule is a fantastic way to automate making that one extra payment each year. Instead of 12 monthly payments, you make 26 half-payments. Because there are 52 weeks in a year, this clever schedule results in 13 full monthly payments by the end of the year.

Let’s look at a real-world scenario. On a $900,000 mortgage at a 6.5% interest rate, switching to a bi-weekly plan from the get-go could help you pay off your loan more than four years earlier and save you over $130,000 in interest. That’s a massive acceleration in your wealth-building journey.

Pro Tip: Before you jump in, call your lender. Some offer this service for free, but others might charge a setup fee. Crucially, you must confirm that any extra funds are being applied directly to your principal balance, not held to be applied to a future payment.

When to Consider Refinancing

Refinancing isn’t just about chasing a lower interest rate; it can be a strategic power play to build equity faster. The most aggressive move is shifting from a 30-year to a 15-year mortgage. Yes, your monthly payment will be higher, but a much larger portion of it attacks the principal from day one, drastically shortening your path to full ownership.

A drop in mortgage rates can create prime refinancing opportunities. Picture this: on an $800,000 single-family home with a 30-year mortgage at 7%, your monthly principal payment might be just $500 at the start. Refinancing to 6% could free up $300 monthly—if you funnel that straight to your principal, you can accelerate your equity buildup by years. You can track these kinds of market trends and their impact on equity on platforms like Rate.com.

Strategic Upgrades That Boost Your Home’s Value

Paying down your mortgage is a guaranteed way to build equity, but let’s be honest—it’s the slow burn. If you want to pour some gasoline on the fire and actively force your home’s value upward, smart upgrades are your best bet.

This isn’t about chasing fleeting design trends from a magazine. It’s about making calculated investments that deliver a real, measurable return. You have to think like a buyer. What updates make a home more functional, more attractive, and ultimately, more valuable in today’s market? Not every project pays for itself, so knowing where to put your money is everything.

Where to Focus Your Renovation Budget

Certain areas of a home consistently punch above their weight when it comes to return on investment (ROI). These are the spaces that can make or break a sale and have the biggest impact on an appraiser’s valuation. Undertaking the right enhancements is a direct way to boost home value and kick your equity growth into high gear.

Here’s where savvy homeowners often start:

- Kitchens and Bathrooms: These are the heart and soul of a home for most buyers. Minor remodels—like refacing cabinets, upgrading to quartz countertops, or installing modern fixtures—can completely change a property’s appeal and recoup a huge portion of their cost. A full gut renovation can be pricey, but in a dated home, it can be the single most impactful project you undertake.

- Curb Appeal: First impressions are everything. You can get a fantastic return from low-cost projects like a new front door, updated exterior paint, modern house numbers, and some thoughtful, low-maintenance landscaping. These upgrades tell buyers the home is well-cared for before they even step inside.

- Creating Functional Space: Adding square footage is often a home run, but it’s expensive. A smarter approach is to better use the space you already have. This could mean finishing a basement, converting an attic into a bonus room, or creating a dedicated home office—a feature that continues to be in high demand.

A common mistake is over-improving for the neighborhood. Before you install a $150,000 chef’s kitchen, make sure the surrounding property values can support that kind of upgrade. Your goal is to meet or slightly exceed neighborhood standards, not to build a palace on a block of bungalows. Working with a real estate professional can provide crucial insight into local market expectations.

The Rise of Smart and Green Upgrades

Today’s buyers are looking for homes that are not just beautiful but also efficient and sustainable. These upgrades can lower utility bills and offer a modern living experience, making them a powerful selling point that really resonates.

Consider these forward-thinking improvements:

- Energy-Efficient Windows: Those old, single-pane windows are an energy vampire. Upgrading to double-pane, low-E windows can slash heating and cooling costs, with some reports showing homeowners can recoup over 60% of the project cost at resale.

- Smart Home Technology: Integrating smart thermostats, lighting, and security systems adds a layer of convenience and modern appeal. These are often relatively low-cost additions that can make your home stand out from the competition.

To dive deeper into projects with proven ROI, explore our guide on how to increase home value before selling, which gets into even more detail.

Comparing Project Costs and Returns

Making an informed decision means looking at the numbers. While costs vary wildly based on your location and the scope of the project, understanding the potential ROI is crucial.

Here’s a look at some popular projects and what you can generally expect.

High-ROI Home Improvements for Today’s Market

| Project | Estimated Cost | Potential ROI (%) | Best For |

|---|---|---|---|

| Minor Kitchen Remodel | $15,000 – $40,000 | 70% – 80% | Homes with a good layout but dated finishes and appliances. |

| Bathroom Remodel | $10,000 – $25,000 | 60% – 70% | Improving a primary or guest bath with modern fixtures and tile. |

| New Garage Door | $2,000 – $5,000 | Over 100% | An incredibly high-impact, low-cost upgrade for instant curb appeal. |

| Exterior Paint | $5,000 – $12,000 | 50% – 60% | Giving the entire property a fresh, clean, and modern look. |

| Outdoor Living Space (Deck/Patio) | $8,000 – $20,000+ | 45% – 65% | Maximizing usable living area, especially in markets with favorable climates. |

Remember, these figures are national averages. The real key to successfully building equity through renovations is to choose projects that align with your local market’s demands and your home’s current condition. What works in one neighborhood might not work in another.

Letting Market Appreciation Do the Heavy Lifting

While you can hustle to pay down your mortgage and renovate for ROI, one of the most powerful wealth-building tools in real estate demands something much simpler: patience.

Market appreciation is the quiet, passive engine that drives your net worth up while you sleep. It’s the magic that happens when your home’s value climbs simply because of where it is and what’s happening around it.

You don’t have to lift a hammer or send an extra dime to the bank. As the market rises, your equity grows right along with it. This is the “work smarter, not harder” side of building wealth through real estate.

What’s Really Driving Your Home’s Value?

Market appreciation isn’t just luck; it’s basic economics playing out in your zip code. It’s the constant dance between supply and demand, and a few key factors almost always lead the choreography:

- Supply and Demand: This is the big one. When more people want to live in an area than there are homes available, prices have a natural tendency to rise.

- Economic Growth: A booming local economy and strong job growth act like a magnet, pulling in new residents who all need a place to live. That surge in demand is a direct catalyst for higher property values.

- Neighborhood Development: Think about that new park, the trendy restaurant that just opened, or a school that’s gaining a strong reputation. These amenities make a neighborhood more desirable, and that desirability translates directly into home value.

You can’t control these larger forces, of course. But what you can control is where you choose to buy. Your initial purchase decision is the single most important move you can make to put the power of appreciation on your side.

How to Position Yourself for Maximum Growth

Winning the appreciation game is all about buying the right property in the right location. It means looking past the fresh paint and new appliances to see the long-term potential of the neighborhood. This is where having a skilled real estate agent is a game-changer.

A seasoned agent doesn’t just see a house; they see its place in the community’s future. They’re tracking zoning changes, city development plans, and infrastructure projects that could completely transform a neighborhood in the next five to ten years.

Choosing a home in an area with a clear path for future growth is like planting a tree in fertile soil. You put it in the ground and let the environment do the heavy lifting for you, allowing your equity to grow naturally over time.

This strategic thinking is what separates a decent investment from a truly great one. It’s not about trying to time the market perfectly—it’s about making a smart, informed decision based on solid, forward-looking data.

The Power of Just Holding On

The impact of appreciation is massive. It’s the simplest way to build wealth: just hold onto your property as the market does its thing. Historical data consistently shows how U.S. house prices have climbed over the long term, turning relatively modest investments into serious wealth. If you want to dig deeper, Amerisave.com explains how rising home values contribute to equity.

Let’s run some simple numbers. Say you buy a home for $800,000. If the local market appreciates by a conservative 5% in one year, your property is now worth $840,000.

That’s $40,000 in equity you gained just by being a homeowner in the right place at the right time. When you add that to the principal you’ve paid down, you start to see how quickly your financial picture can change. It’s a powerful lesson in how to build equity in your home with a long-term mindset.

Putting Your Home Equity to Work

You’ve done the hard work. You’ve been hammering away at that principal, making smart upgrades, and letting the market do its thing. Now for the fun part: figuring out what all that hard-earned equity can actually do for you.

Think of your equity as a launchpad. It’s stored financial energy you can deploy to hit bigger goals, whether that’s grabbing an investment property, wiping out high-interest debt, or just climbing the property ladder. This isn’t just a number on paper; it’s a dynamic asset ready for action.

Tracking Your Progress and Planning Your Next Move

First things first, you have to know your numbers. You should be checking your home’s estimated market value at least once or twice a year and watching that mortgage balance shrink on your statements. It’s the only way to know when you have enough skin in the game to make a real move.

Once you have a clear picture, you can start identifying opportunities. Has your equity grown enough to consider one of these power plays?

- Selling to Capitalize: This is the most direct route. Cashing out your equity by selling gives you a lump sum to roll into your next home or another investment entirely. It’s clean and straightforward.

- Leveraging for Another Purchase: This is where things get interesting. Using a home equity loan or HELOC can provide the down payment for another property, expanding your real estate portfolio without selling your primary residence. If you’re fuzzy on the details, our guide on what a home equity loan is breaks it all down.

- Refinancing to Invest: A cash-out refi can turn that paper equity into liquid funds for other ventures. We’ve seen clients use this money to invest in the stock market, start a business, or fund a major renovation.

Building wealth through real estate is a long game. The key is to see your home not just as a place to live, but as the cornerstone of your financial strategy. Each decision should be a deliberate step toward your next goal.

When to Bring in the Professionals

Making big money moves requires a solid game plan backed by people who know what they’re doing. Before you tap into your equity, talking to the right professionals is non-negotiable.

A real estate agent provides the essential market analysis, showing you what your home is truly worth and what the market will bear right now. Not a website estimate, but what actual buyers are paying.

To really understand how to turn that equity into usable cash, exploring options like refinancing a property is a critical step. At ACME Real Estate, we can connect you with trusted financial advisors who live and breathe this stuff. They’ll help you weigh the pros and cons to make sure your next move is the right one for your long-term goals.

Common Questions About Building Home Equity

We’ve covered a lot of ground—from aggressive mortgage pay-downs to smart, value-adding renovations. But theory is one thing, and your specific situation is another. You probably still have some questions buzzing around.

Let’s tackle those common “what ifs” and “should Is” head-on. Here are the clear, straightforward answers to the questions homeowners ask us most on their equity-building journey.

How Long Does It Take to Build Significant Equity?

This is the million-dollar question, and the honest answer is: it depends. There’s no magic number. Your path to building a real stake in your property is a mix of your own financial discipline and the whims of the market.

In the early years of a typical 30-year mortgage, it can feel like you’re just treading water. Most of your monthly payment gets eaten up by interest, with only a tiny fraction chipping away at the principal. Because of how amortization works, you really start to see equity growth from payments alone accelerate after the five-to-seven-year mark.

But market appreciation is the ultimate wild card. A hot market can do more for your equity in two years than your payments might do in ten. Homeowners in various parts of the country in recent years saw their equity explode thanks to rapid price jumps, not just their mortgage payments.

The fastest way to jumpstart your equity is with a substantial down payment. Putting 20% or more down gives you an immediate, significant cushion from day one. It’s like starting a race halfway to the finish line.

Ultimately, your timeline is a blend of these factors:

- Your Down Payment: A bigger initial stake means more equity from the jump.

- Your Loan Term: A 15-year mortgage builds equity exponentially faster than a 30-year loan.

- Market Conditions: A rising tide lifts all boats, and a rising market can create huge equity in just a few years.

- Extra Payments: Consistently paying more than your minimum shaves years off your loan and fast-tracks equity growth.

The key is to control what you can—your payments—while setting yourself up to benefit from what you can’t control.

Should I Make Home Improvements or Extra Mortgage Payments?

This is the classic homeowner’s dilemma. Do you invest in your property or invest in paying it off faster? One offers a guaranteed, safe return; the other offers the potential for a much bigger payoff, but with more risk.

The right choice comes down to your financial situation, your goals, and your home’s current state.

Making extra mortgage payments is a risk-free win. The return on that money is equal to your mortgage interest rate. If your rate is 6.5%, every extra dollar you pay toward the principal is essentially earning you a guaranteed 6.5% return because it’s interest you no longer have to pay. It’s the slow, steady, and certain path.

Home improvements are speculative. A killer kitchen remodel could deliver a 75% return on investment, meaning you get back $0.75 in added home value for every dollar spent. That’s a fantastic return, but it’s never a sure thing. Costs can get out of hand, trends change, and the final value is ultimately decided by the market and an appraiser.

Here’s a simple framework to help you decide:

- Check Your Financial Health: Do you have a solid emergency fund (3-6 months of expenses)? Are you saving for retirement? If your financial foundation isn’t rock-solid, focus on the guaranteed return of paying down your mortgage.

- Assess Your Home’s Needs: Is your place seriously dated compared to other homes in the neighborhood? If a tired kitchen or an ancient bathroom is actively dragging down your property’s value, a renovation might be the more powerful move.

- Consider Your Timeline: If you plan to sell in the next few years, a high-ROI renovation could seriously boost your sale price. If you’re staying put for the long haul, the interest savings from extra payments might be more appealing.

Think of it this way: extra payments are like buying a high-quality bond, while renovations are like investing in a growth stock. Both can be smart moves, but they serve different purposes.

What Are the Biggest Mistakes to Avoid?

Knowing how to build equity is only half the battle. Knowing what not to do is just as important. A few common missteps can quietly sabotage your progress, erasing hard-earned gains before you even realize it.

One of the most common errors is over-improving for the neighborhood. It’s tempting to build your dream kitchen, but sinking $200,000 into a renovation in an area where homes top out at $900,000 means you’ll never see a full return on that money. The goal is to bring your home in line with the top of the local market, not to blow past it.

Another major mistake is treating a Home Equity Line of Credit (HELOC) like a personal ATM for vacations and new cars. Using your equity to pay for depreciating assets is a surefire way to destroy the wealth you’ve worked so hard to build. Full stop.

Here are a few other common traps to sidestep:

- Neglecting Basic Maintenance: It’s not sexy, but a leaky roof, bad plumbing, or peeling paint will actively decrease your home’s value. Deferred maintenance is a silent equity killer.

- Forgetting About PMI: If you put down less than 20%, you’re paying Private Mortgage Insurance. Once your equity hits 20-22% (through payments and appreciation), you can request to have it removed. Forgetting to do this is just throwing money away every month.

- Choosing the Wrong Renovations: Not all improvements are created equal. Adding a swimming pool might sound amazing, but in many markets, it has a notoriously low ROI. Stick to projects with proven appeal, like updated kitchens, modern bathrooms, and curb appeal.

Avoiding these mistakes ensures your efforts are always moving you forward, steadily turning your home into the powerful financial engine it’s meant to be.

Building home equity is a marathon, not a sprint. It takes a smart strategy, consistent action, and a clear vision. Whether you have more questions or you’re ready to put your equity to work, our team at ACME Real Estate is here with the local expertise you need to make your next move.

Ready to explore your options in the Los Angeles market? Contact us today and let’s build your wealth together.