That feeling when the sale closes is epic. But the tax bill that follows? Not so much. Selling real estate, especially in a dynamic market like Los Angeles, often comes with a hefty side of real estate capital gains tax. This isn’t just some minor line item; it’s a beast that can take a serious bite out of the profits you’ve worked hard to build, whether you’re an investor, a home flipper, or just sold your family home. Think of it as the government’s slice of your investment success pie.

But here’s the deal: many savvy property owners and investors don’t pay the full sticker price. Why? Because they know the game. The U.S. tax code is packed with powerful, 100% legal strategies designed to defer, reduce, or even completely wipe out this tax. It’s not about dodging your responsibilities; it’s about playing chess, not checkers, with your finances.

This isn’t just for the mega-rich or corporate giants. Whether you’re selling your primary residence or offloading an investment property, understanding these strategies is your ticket to maximizing your return. This guide moves beyond the basics to give you a clear, actionable playbook. We’re about to break down 8 powerhouse methods that can save you thousands, or even millions. From the well-known primary residence exclusion to more advanced techniques like Opportunity Zone investments and Delaware Statutory Trusts, we’ll cover the tools you need to protect your profits. Let’s get into it, but please cross check all of this information with an accountant. We are not accountants and are not representing that we are!

1. The Investor’s Power Move: The 1031 Like-Kind Exchange

For savvy real estate investors, the 1031 like-kind exchange is less of a loophole and more of a superhighway to building generational wealth. Governed by Section 1031 of the IRS code, this powerful tool allows you to defer paying real estate capital gains tax when you sell an investment property, provided you reinvest the proceeds into a new, “like-kind” property of equal or greater value.

Instead of forking over a significant chunk of your profit to the government, you roll your entire equity into the next deal. This isn’t tax avoidance; it’s a strategic deferral that lets your investment growth compound without the tax drag slowing you down. Think of it as telling the IRS, “I’m not cashing out; I’m trading up.”

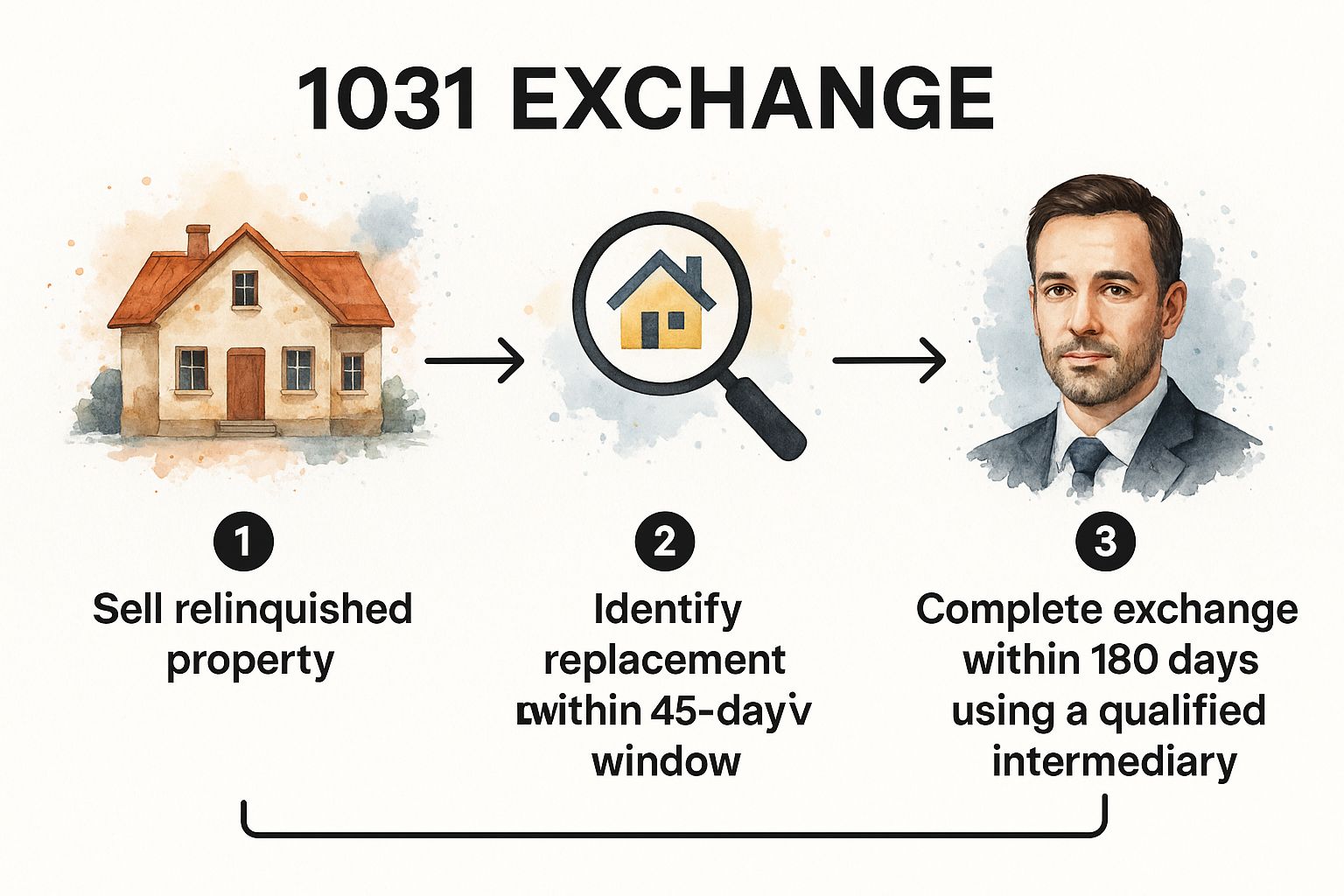

How a 1031 Exchange Works

The magic of a 1031 exchange lies in its strict but straightforward rules. You’re not just selling one property and buying another. The process requires a Qualified Intermediary (QI) to hold the funds from the sale of your initial property (the “relinquished” property) and use them to acquire your new one (the “replacement” property).

For example, an investor in Los Angeles sells a $1 million duplex and uses a 1031 exchange to acquire a $1.2 million four-plex, deferring all capital gains tax on the sale. This allows them to leverage their full equity to increase their door count and potential cash flow. The key is that the properties must be held for business or investment purposes, but “like-kind” is defined very broadly. You can exchange raw land for a commercial building or a single-family rental for an apartment complex.

Navigating the Strict Timelines

The 1031 exchange process is governed by two critical and non-negotiable deadlines that begin the day you close on your relinquished property.

- 45-Day Identification Period: You have 45 calendar days to formally identify potential replacement properties in writing to your QI. You can typically identify up to three properties of any value.

- 180-Day Exchange Period: You must close on one or more of your identified replacement properties within 180 calendar days of the original sale.

The following infographic illustrates this critical workflow.

As the diagram shows, these deadlines run concurrently, making pre-planning essential for a successful exchange.

The 1031 exchange is just one of several powerful strategies available to investors. To explore a comprehensive list, you can learn more about other real estate investment tax benefits and how they can complement your portfolio growth.

2. Primary Residence Exclusion (Section 121)

For most homeowners, the Primary Residence Exclusion is the single most valuable tax benefit available. Governed by Section 121 of the IRS tax code, this powerful provision lets you exclude a massive amount of profit from taxation when you sell your main home. Eligible single filers can exclude up to $250,000 in capital gains, and that figure doubles to a staggering $500,000 for married couples filing jointly.

Unlike the 1031 exchange, which defers taxes, this is a true exclusion—the profit is yours to keep, tax-free. You don’t need to reinvest the proceeds into another property. This rule turns your home into a powerful wealth-building tool, rewarding you for the equity you’ve built over the years and letting you completely sidestep real estate capital gains tax on a huge portion of your sale.

How the Primary Residence Exclusion Works

Qualifying for this tax break hinges on two simple but crucial tests: the Ownership Test and the Use Test. You must have both owned the home and lived in it as your primary residence for at least two of the five years leading up to the sale date. These two years do not need to be continuous.

For example, a married couple in Los Angeles buys a home for $300,000. They live there for three years, make some improvements, and sell it for $750,000. Their total capital gain is $450,000. Because they meet both the ownership and use tests and are under the $500,000 exclusion limit for joint filers, they pay zero capital gains tax on the sale. This strategy is also a favorite of savvy house flippers who live in a property long enough to qualify before selling.

Navigating the Key Requirements

While powerful, the exclusion comes with specific rules. Meticulous planning and record-keeping are your best friends.

- Two-Year Use Rule: You can generally only use this exclusion once every two years.

- Partial Exclusions: If you fail to meet the two-year requirement due to unforeseen circumstances like a job change, health issues, or military deployment, you may still qualify for a partial or prorated exclusion.

- Record Keeping: Keep detailed records of your home’s purchase price, sale price, and any capital improvements made. These improvements increase your cost basis, which shrinks your total capital gain.

Understanding these rules is key to maximizing your tax-free profit, a concept just as important as knowing how local regulations affect your bottom line. To get a complete picture, it’s wise to learn more about other property-related finances like property taxes in Los Angeles to fully prepare for homeownership.

3. The Installment Sale Method

For sellers who prefer a steady income stream over a single lump-sum payday, the installment sale method offers a slick way to manage your real estate capital gains tax liability. This strategy allows you to sell a property but receive payments from the buyer over a set period. Instead of paying tax on the entire gain in the year of the sale, you pay it in pieces as you receive payments.

This approach effectively spreads the tax impact over multiple years, which can keep you in a lower income tax bracket. Rather than facing a massive tax bill all at once, you’re creating a more predictable and manageable financial future. Think of it as turning a large, taxable event into a multi-year income plan.

How an Installment Sale Works

The core of an installment sale is recognizing your profit proportionally. The IRS lets you calculate a “gross profit percentage” for the sale. Each year, you apply this percentage to the principal portion of the payments you receive to determine how much of your gain is taxable for that year. This method is particularly useful for sellers who don’t need all the cash upfront.

For example, a retiree sells an $800,000 investment property with a $600,000 capital gain. Instead of a cash sale, they structure an installment sale over 10 years. This lets them recognize just $60,000 of the gain each year, potentially keeping them in a lower tax bracket and significantly reducing their total tax burden over the life of the agreement. Similarly, a business owner could use this to sell a commercial building to a key employee over a 15-year period, facilitating a smooth ownership transition.

Key Considerations for a Successful Sale

While powerful, an installment sale introduces the risk of buyer default. To protect your interests, it’s crucial to structure the deal like a fortress.

- Secure a Strong Down Payment: Require a substantial down payment to ensure the buyer has significant skin in the game, reducing the likelihood of default.

- Implement Protective Clauses: Include personal guarantees or other forms of collateral in the sale agreement to provide recourse if the buyer fails to pay.

- Vet Your Buyer: Prioritize selling to financially stable buyers with a proven track record to minimize risk over the long term.

- Plan for Inflation: For long-term contracts, consider building in interest rate adjustments to protect the real value of your future payments.

This strategy is a fantastic tool for estate planning, business succession, and for any seller looking to defer gains and create a reliable income stream.

4. Opportunity Zone Investment

For investors looking for both significant tax benefits and a way to make a tangible impact, Opportunity Zones present a unique and compelling strategy. Established by the 2017 Tax Cuts and Jobs Act, this program encourages long-term investment in economically developing communities. It allows you to defer and even reduce your real estate capital gains tax by reinvesting gains from almost any asset sale into a Qualified Opportunity Fund (QOF).

This isn’t just a tax play; it’s a dual-purpose strategy that directs capital toward areas in need of revitalization while offering powerful incentives. Instead of just handing over a check to the tax man on your profits, you can put that capital to work, fostering economic growth and potentially generating new, tax-free returns for yourself.

How Opportunity Zone Investing Works

The heart of the Opportunity Zone program is reinvesting eligible capital gains into a QOF within 180 days of the sale. These funds then deploy capital into designated low-income census tracts by funding real estate projects or operating businesses. Unlike a 1031 exchange, the source of the capital gain can be from the sale of stocks, a business, or real estate.

For example, a tech entrepreneur in California sells $2 million in company stock. Instead of paying capital gains tax, they invest the entire gain into a QOF that is developing a mixed-use commercial and residential project in a designated Opportunity Zone. By doing so, they defer the initial tax liability and position themselves for future tax-free growth on the new investment. The benefits are tiered and reward long-term commitment.

Navigating the Key Timelines and Benefits

The power of Opportunity Zone investing is unlocked over time, with benefits accumulating based on your holding period.

- Tax Deferral: You defer paying capital gains tax on the initial invested amount until December 31, 2026, or until you sell your QOF investment, whichever comes first.

- Tax Elimination: The biggest prize comes from holding the QOF investment for at least 10 years. If you do, any appreciation on the QOF investment itself is completely tax-free upon sale.

This 10-year hold is the holy grail of the program, offering a path to eliminate future capital gains entirely. For more information on qualifying funds and locations, you can explore the official IRS guidelines and resources.

5. Tax Loss Harvesting with Real Estate

While often discussed in the stock market, tax loss harvesting is a sophisticated move that savvy real estate investors can use to minimize their tax bill. This approach involves strategically selling underperforming properties at a loss to offset capital gains from your profitable sales, effectively lowering your overall real estate capital gains tax liability for the year.

Instead of letting a struggling asset drag down your portfolio’s performance, you can turn its poor performance into a direct tax advantage. This isn’t about giving up on an investment; it’s about making a calculated financial decision to realize a loss that can shelter your hard-earned gains from the taxman. Think of it as pruning your portfolio to encourage healthier, more tax-efficient growth.

How Tax Loss Harvesting Works

The core principle is simple: capital losses cancel out capital gains. If you have gains from selling a successful investment property, you can sell another property that has decreased in value to generate a capital loss. The IRS allows you to use these losses to offset your gains on a dollar-for-dollar basis.

For instance, a developer sells a completed residential project and realizes a $200,000 capital gain. In the same year, they sell a stalled commercial project at a $150,000 loss. The developer can use the $150,000 loss to offset the gain, meaning they only owe capital gains tax on the remaining $50,000 profit. This strategic sale transforms a portfolio weak spot into a significant tax shield.

Navigating Key Considerations

While the “wash sale” rule that applies to stocks doesn’t apply to real estate, investors still must be careful. The IRS has rules about selling to related parties, so you can’t just sell a losing property to a family member to book the loss and keep it in the family. Strategic timing and careful planning are crucial.

- Plan Near Year-End: Many investors review their portfolios in the fourth quarter to identify opportunities for loss harvesting before the tax year closes.

- Maintain Meticulous Records: Keep detailed documentation of purchase prices, sale prices, and all associated costs for both the profitable and losing properties.

- Assess Market Conditions: Before selling, consider the property’s future potential. Is it a temporary dip or a long-term decline? Ensure the tax benefit outweighs the potential for a future rebound.

- Coordinate with Other Strategies: Tax loss harvesting works best when integrated with a broader tax planning strategy, complementing tools like 1031 exchanges or opportunity zone investments.

6. Conservation Easement Donation

A conservation easement donation is a unique and altruistic strategy for landowners looking to preserve their property’s natural or historical character while gaining a significant tax advantage. It involves voluntarily and permanently restricting development rights on your land and donating those rights to a qualified conservation organization, such as a land trust. While you still own the land, you’ve ensured it will remain undeveloped for future generations.

This isn’t a direct way to avoid real estate capital gains tax, but it creates a substantial charitable income tax deduction. This deduction, based on the appraised value of the donated development rights, can be used to offset income from other sources, including capital gains from selling other real estate assets. It’s a powerful tool for those who prioritize legacy and land stewardship alongside financial planning.

How a Conservation Easement Works

The core of this strategy lies in valuing the “lost” development potential of your property. A qualified appraiser determines the land’s fair market value both with and without the development restrictions. The difference between these two values is the value of your charitable donation, which you can then deduct from your taxable income.

For example, a rancher in a rapidly developing area owns 500 acres. By donating the development rights to a local land trust, they prevent the land from ever being subdivided for housing. If the appraiser values the land at $3 million with development potential and $2 million without it, the rancher receives a $1 million charitable deduction. This deduction can be used to significantly lower their overall tax liability in the year of the donation and can often be carried forward for several years.

Key Considerations and Best Practices

Executing a conservation easement donation requires careful planning and professional guidance to ensure it aligns with both your financial and conservation goals. The restrictions are permanent and bind all future owners of the property.

- Find a Qualified Appraiser: Work with an appraiser who has specific experience valuing conservation easements to ensure the donation meets IRS requirements.

- Partner with a Reputable Land Trust: Choose an established and accredited conservation organization to hold and enforce the easement in perpetuity.

- Understand the Permanence: The restrictions you place on the land are forever. This decision will impact your family’s future use of the property and its market value.

- Confirm Conservation Value: The property must have legitimate conservation value, such as providing a wildlife habitat, scenic views, or preserving historic farmland, to qualify for the tax deduction.

This approach is ideal for landowners who are more motivated by conservation and legacy than by maximizing development profit. It allows you to protect the land you love while receiving a powerful tax benefit that can offset other financial events, including significant capital gains.

7. Qualified Small Business Stock (QSBS) Election

While often associated with tech startups, the Qualified Small Business Stock (QSBS) election is a game-changing, yet lesser-known, strategy for real estate entrepreneurs. Governed by Section 1202 of the IRS code, this provision allows investors to exclude up to 100% of their capital gains from the sale of qualifying stock, capped at $10 million or 10 times the stock’s basis, whichever is greater. This isn’t just a minor deduction; it’s a potential complete wipeout of your real estate capital gains tax liability.

This powerful tool is available to those who invest in or operate a real estate business structured as a C corporation. Instead of selling property directly, you’re selling your equity in the company that owns the real estate assets. For founders and early investors in qualifying real estate ventures, this can translate into millions of dollars in tax savings, providing a massive incentive to structure businesses for growth from day one.

How a QSBS Election Works

The magic of QSBS hinges on meeting several strict criteria, but the payoff is immense. The business must be a domestic C corporation with gross assets of $50 million or less at the time the stock is issued. Critically, the corporation must also meet an “active business” requirement, meaning at least 80% of its assets are used in the operation of a qualified trade or business, which can include real estate development or management.

For example, a founder of a real estate development company in Los Angeles, structured as a C corporation, invests an initial $500,000. After six years, the company is acquired by a larger firm, and her shares are worth $8 million. Because she held the QSBS-qualified stock for more than five years, she can exclude the entire $7.5 million capital gain from her taxes, saving millions. The key is that the stock, not the individual properties, is being sold.

Navigating the QSBS Requirements

Successfully leveraging the QSBS election requires meticulous planning and documentation from the very beginning. Unlike other strategies, this isn’t something you can decide on at the time of sale; the business must be structured correctly from its inception.

- Proper Entity Structure: The business must be a C corporation. S corporations and LLCs do not qualify, so this decision must be made early.

- Five-Year Holding Period: You must hold the stock for more than five years to qualify for the full 100% gain exclusion.

- Asset and Business Tests: The company must continuously meet the $50 million gross asset test and the 80% active business requirement. This demands diligent record-keeping of asset values and business activities.

For high-growth real estate ventures, from development firms to tech-enabled property management companies, the QSBS election offers a path to a tax-free exit that few other strategies can match.

8. Delaware Statutory Trust (DST) Investment

For investors craving a hands-off approach to deferring capital gains, the Delaware Statutory Trust (DST) offers an elegant and powerful solution. A DST allows you to own a fractional, passive interest in a large portfolio of institutional-grade real estate. This structure is recognized by the IRS as “like-kind” property, making it a popular and efficient vehicle for completing a 1031 exchange.

Instead of hunting for a replacement property yourself, you invest your sale proceeds into a professionally managed DST. This strategy effectively eliminates the burdens of direct ownership while allowing you to defer your real estate capital gains tax. Think of it as trading the headaches of being a landlord for the benefits of being a passive, institutional investor.

How a DST Works

A DST is a legal entity that holds title to one or more income-producing commercial properties. A “sponsor” company acquires the properties, structures the DST, and offers fractional interests to investors. As an investor, you become a beneficiary of the trust, entitling you to a share of the property’s income and potential appreciation without any day-to-day management responsibilities.

For example, a retiring landlord in Los Angeles sells a $2 million apartment building and uses a 1031 exchange to invest the proceeds into a DST that owns a portfolio of medical office buildings and distribution centers across the country. They successfully defer all capital gains, diversify their holdings, and begin receiving passive monthly income without ever having to deal with another tenant call.

Navigating DST Investments

While DSTs simplify the 1031 exchange process, especially for investors struggling to meet the 45-day identification deadline, due diligence is critical. Choosing the right sponsor and understanding the investment’s nuances are key to a successful outcome.

- Sponsor Track Record: Thoroughly research the sponsor’s history, experience, and performance on past deals. A proven track record is your best indicator of future success.

- Understand the Fees: Be crystal clear on all upfront fees, ongoing management costs, and compensation structures. These expenses directly impact your net returns.

- Review Property Details: Even as a passive investor, you should carefully review the underlying property’s financials, tenant roster, lease terms, and market conditions.

- Acknowledge Illiquidity: DST investments are long-term and generally illiquid. Be prepared to hold your interest for the planned duration, which is often 5-10 years.

DSTs provide a strategic path to passive real estate ownership and tax deferral. To better understand the financial structuring behind such large-scale acquisitions, you can explore how to finance investment property and the methods sponsors use.

Real Estate Capital Gains Tax: Strategy Comparison

| Strategy | Implementation Complexity 🔄 | Resource Requirements ⚡ | Expected Outcomes 📊 | Ideal Use Cases 💡 | Key Advantages ⭐ |

|---|---|---|---|---|---|

| 1031 Like-Kind Exchange | High – strict timelines, legal docs | Moderate – qualified intermediary fees | Tax deferral, reinvest full equity | Real estate investors seeking tax deferral | Complete capital gains deferral; repeatable |

| Primary Residence Exclusion | Low – simple qualification | Low – personal records maintenance | Tax-free capital gains up to limits | Homeowners selling primary residence | Fully tax-exempt gains within limits; repeatable |

| Installment Sale Method | Moderate – contract structuring | Moderate – legal and financial advice | Spread gains over years; steady income | Sellers needing tax smoothing and income stream | Reduce immediate tax burden; flexible payments |

| Opportunity Zone Investment | High – compliance, long-term hold | High – QOF investment management | Deferred and reduced capital gains tax | Investors aiming for community impact + tax benefits | Tax deferral + elimination; supports distressed areas |

| Tax Loss Harvesting with Real Estate | Moderate – timing and portfolio management | Low to moderate – transaction costs | Capital loss offsets reducing tax load | Investors with underperforming properties | Offset gains, flexible timing, no wash sale rule |

| Conservation Easement Donation | High – appraisal, legal restrictions | Moderate – appraisal and legal fees | Charitable deductions, estate tax benefits | Landowners seeking tax deductions + conservation | Significant charitable deduction; land preservation |

| Qualified Small Business Stock Election (QSBS) | High – strict business and holding criteria | Moderate – entity structure and compliance | Large gain exclusions | Investors in qualifying small C corp businesses | Up to $10M gain exclusion; encourages small biz investment |

| Delaware Statutory Trust (DST) Investment | Moderate – passive investment setup | Moderate to high – minimum investment | Passive income + 1031 exchange eligibility | Investors seeking passive commercial real estate | Access institutional properties; management handled |

Your Next Move: Turning Tax Strategy into Reality

Navigating the landscape of real estate capital gains tax can feel like trying to solve a complex puzzle with missing pieces. But as we’ve explored, understanding the rules of the game is the first step toward winning it. This isn’t about finding shady loopholes; it’s about leveraging legitimate, powerful strategies the tax code provides for savvy property owners and investors just like you. The key is to shift your mindset from reacting to a tax bill to proactively shaping it.

The strategies we’ve detailed—from the homeowner-friendly Primary Residence Exclusion to the investor-centric 1031 Exchange—are not just abstract financial theories. They are tangible tools. Think of them as a specialized toolkit where each tool is designed for a specific job. Selling your long-time family home in Los Angeles is a completely different scenario than deferring gains from a rental property portfolio, and your tax strategy needs to reflect that nuance.

From Knowledge to Action: Your Implementation Checklist

The most significant takeaway is that the moment of sale is too late to start planning. Strategic tax management begins long before your property is listed. To help you transition from reading this article to taking concrete steps, here is a practical checklist to guide your next move:

- Review Your Goals: Before you even think about which strategy to use, clarify your objectives. Are you looking to cash out completely? Reinvest in a bigger or different type of property? Diversify your assets? Your ultimate goal will dictate the most appropriate tax-deferral or exclusion strategy.

- Document Everything: Meticulous record-keeping is your best defense against overpaying on your real estate capital gains tax. Start compiling receipts for all capital improvements now. That new roof, remodeled kitchen, or backyard landscaping project could significantly increase your cost basis and lower your taxable gain.

- Assemble Your Professional Team: Your real estate agent is your market expert, but they are just one part of your A-team. You also need a qualified tax professional (like a CPA) and potentially a financial advisor. Engage them early in the process. Ask them specific questions like, “Given my AGI and the sale price, how would an installment sale affect my tax bracket over the next few years?” or “Does a DST investment align with my long-term liquidity needs?”

- Timeline Your Strategy: Certain strategies have strict deadlines. The 1031 exchange, with its 45-day identification and 180-day closing periods, is the most notorious. But even strategies like Opportunity Zone investments have timelines for reinvesting your capital gains. Map these dates out to ensure you don’t miss a critical window.

The True Value of Strategic Tax Planning

Mastering the concepts of real estate capital gains tax does more than just save you money on a single transaction. It fundamentally changes how you view your real estate assets. Instead of seeing them as just a place to live or a simple investment, you begin to see them as dynamic financial instruments with immense potential for wealth creation and preservation.

Key Insight: Effective tax strategy isn’t a one-time event; it’s an integral part of your entire real estate investment lifecycle. The decisions you make today will directly impact your financial flexibility and legacy for years to come.

Whether you’re a first-time seller in Los Angeles benefiting from the $250,000 or $500,000 primary residence exclusion or a seasoned investor rolling gains into a Delaware Statutory Trust, the principle is the same. You are in control. By understanding these rules, you empower yourself to keep more of your hard-earned equity working for you, building a stronger financial future one smart move at a time.

Navigating the complexities of a real estate transaction, especially with the significant financial implications of capital gains tax, requires more than just market knowledge. At ACME Real Estate, we connect our clients with a network of trusted tax professionals and financial advisors to ensure every sale is structured for maximum benefit. Let us help you assemble the right team and build a winning strategy for your property.